TransDigm & PMAs, CCC vs Mitchell Casualty, Toast Gross Churn

Published Last Week

Two months ago, TransDigm acquired Jet Parts Engineering and Victor Sierra for $2.2bn. Historically, TransDigm acquired sole or limited source proprietary OEM parts. This acquisition marked the first move into acquiring test and computation PMAs, or reverse-engineered OEM parts.

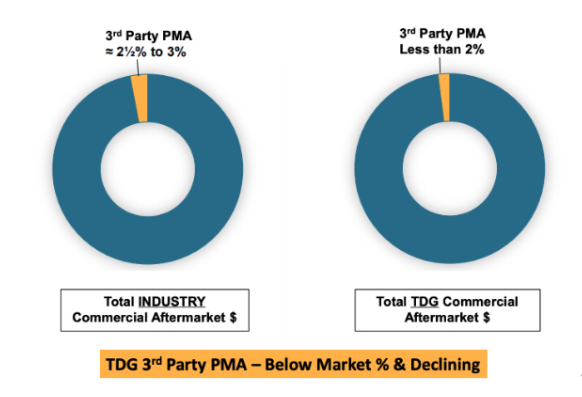

PMA parts are typically seen as a threat to the core of TransDigm’s portfolio. Companies such as HEICO, Wencor, and Jet Parts reverse-engineer OEM parts to identical or improved fit, form, and function, and offer the PMA at a 30-40% discount to OEM prices (whilst still earning 60%+ gross margins). PMAs aim to save airlines money on maintenance. Whilst attractive to airlines, TransDigm has reported that PMA isn't a significant risk:

TransDigm has over 300,000 part numbers. It estimates ~130 T&C PMAs are filed each year on its products. Even if these part numbers completely replaced the TDG OEM part, it seems a minor risk. There are multiple reasons why TransDigm is relatively protected from PMAs:

- 90%+ of TDG parts are below $5,000 per unit and are mission critical.

- On average, it takes ~1.5 years and ~$100k per part to approve a PMA.

- TDG parts are often complex assemblies, not single components.

- Aircraft lessors contractually prohibit airlines from returning aircraft or engines with PMA parts (one reason why FTAI created a SPV to acquire engines at scale).

- Not only do PMA companies need FAA approval for a T&C PMA, but the airline has a separate internal approval process.

All of these factors combine to protect TDG positioning versus PMA.

TransDigm's acquisition of Jet Parts is particularly interesting given the potential organic growth opportunity in PMA’ing competitor products. TransDigm is no stranger to this. The company has been working with PMA shops for years. But having Jet Parts’ capabilities in-house will strengthen TransDigm’s portfolio. It can now plug gaps in its offering by PMA’ing competitor products without leaning on HEICO or Wencor.

We actually PMA'd some of our competitors' stuff where there was one part that was always getting smashed and had a lot of volume. - Former President at TransDigm

This interview with a Former Jet Parts senior executive explores TransDigm’s post-acquisition opportunity:

One of the types of parts that are important to engines that TransDigm makes OEM parts for is EGT sensors... I wanted to try to get them to work with us to PMA their competitor's part... But I would not be surprised if Jet Parts starts getting into PMAing EGT probes and EGT harnesses, thermocouples and harnesses. That would be something that, if I was John Benchite, the president of Jet Parts, as soon as the deal is done, I would go up to management. I would say, "Listen, can these guys help us with reverse engineering the competitor EGT probes and EGT harnesses?" - Former Director at Boeing & Jet Parts Engineering

TDG’s experience and understanding of OEM volume demand and part profit pools may help target new PMAs:

You know what you can sell it for, usually 50%, 60%, 65% of the OEM price. You know what your manufacturing cost is. A very important piece is how many pieces a year are you going to sell? What's the usage at that airline that you're working with? You can get that from the OEM sister company because the OEM sister company knows what the usage is of their competitors. - Former Director at Boeing & Jet Parts Engineering

While this transaction shouldn’t necessarily be seen as a large strategic shift away from its core business, it does highlight the law of large numbers weighing on the company. There just aren’t that many acquisition targets that can move the needle.

This interview can be read alongside the following:

CCC provides software to auto insurers and repair shops to increase accuracy, speed, and reduce the cost of estimating claims. Mitchell is its largest US competitor. They are astutely positioned: CCC has an estimated ~80% share of auto physical damage claims; Mitchell has estimated ~80% share of casualty claims. Late last year, CCC acquired EvolutionIQ to push further into first and third-party injury claims to compete with Mitchell in casualty.

As part of our ongoing CCC coverage, we interviewed a Former Head of Claims at GEICO, who has used and acquired solutions from both companies, to explore the differences in the auto and casualty claims process.

CCC reports that bodily injury claims account for 52% of total liability dollars paid, despite only one in four property damage exposures carrying an associated BI claim. This is due to the cost inflation in medical and lawyer costs:

A CAT scan is medical technology that has been in existence for many decades, going back to the 1970s and 1980s. In 2019, the year before Covid, doctors were recommending 2.51 CAT scans on average per injured party. That increased to 2.73, which is a 9% increase in the average number of unique CAT scans per injured party. Now look at the amounts charged. This is old technology, not an MRI or open MRI. The amount charged is up 43%. When I talk about it being a cottage industry, it really is; people are looking to get more money out of insurance companies. That's the amount charged, not the amount paid, but it gives you an idea of what happens. - Former SVP of Claims at GEICO

The average third-party bodily injury claim is ~$30,000 compared to $4,800 average auto repair cost. Of the ~$30k liability claim, ~30% is for general, “pain and suffering” damages. These are subjective damages and based on the insurer’s judgement.

General damages are pain and suffering. Pain and suffering is: Wes likes to play tennis, and he couldn't play tennis for three months because of injury. That is more subjective. You and I could look at the same case, and you could say, because you're brilliant and disciplined, it's not that big of a deal; the pain and suffering amount for this claim is $3,000. I might be a little less focused and disciplined, and I might say it's $7,000. You can have some impact on all of those things. You're trying to guard against abuse throughout the claims department and pay every nickel you owe and not a nickel less, but not a nickel more either…The insurance company needs consistency. - Former SVP of Claims at GEICO

Auto physical damage claims require little judgement; labour hours and part costs are known.

How much of the auto physical damage claim is judgment? The only thing that's judgment is if the part can be repaired. Am I paying three hours of labor or am I paying the labor? Those are hours of labor, and each hour of labor is worth $70; it's just not that big of a deal. - Former SVP of Claims at GEICO

The casualty workflow is more desk-based and requires careful review of hundreds of medical documents. While CCC’s AI processing tool can provide an initial estimate, 20% of the average physical damage claim is a supplement added once the repair shop tears down the car. There is only so much you can see from outside the vehicle.

There's a lot of time spent reading and reviewing records in casualty. It's more of a desk job, and AI is going to have a greater impact on desk-oriented tasks as opposed to other work. AI is already having an impact on the physical damage side, but over time it will have a more profound impact on casualty than on autophysical damage. It's important on autophysical damage. Let's finish liability before we go to autophysical. - Former SVP of Claims at GEICO

The size of the claims, subjectivity, and desk-based, document-heavy claims process suggests the casualty claims workflow is suited to AI-based estimatics solutions. Switching costs on casualty also seem higher:

The switching costs on casualty are going to be much higher than the switching costs on auto. There are just more moving pieces; there are injury claims. So much of what happens is medically based, and medicine evolves at a totally different rate. The abuse is different. I mean injections and surgeries and diagnosis codes; it's just different than a fender that's dented and needs to be repaired or replaced…if you think about it, when it comes to auto physical damage, the cost of the parts and the amount of labor are all driven by published materials; there's not that much left for judgment. When it comes to a third-party medical claim, there's a ton of judgment involved. Things that you can do to get consistency on the application of judgment and on the cost of the claim help the insurer control that payment. - Former SVP of Claims at GEICO

CCC’s stock is down 50% since listing. It has 99% GRR, is profitable but levered, and is growing ~11% per year. We will be studying EvolutionIQ and CCC’s auto physical and casualty opportunities in more detail this year. This interview can be read alongside the following:

In Q2 24, Toast reported ~10% annual churn. Around 30-40% of churn is from restaurants going out of business. 6-7% annual churn is excluding bankruptcies. NRR is consistently 110%+. As part of our ongoing vertical market software coverage, we published four interviews on Toast last week. A common thread between all interviews led to an interesting observation: Toast's historical churn challenge has never been a competitive issue, it comes from customers trading down from modules purchased but never activated. A Former Director of Strategy & Operations at Toast, who reported directly to COO (now CEO) Aman Narang, highlights:

Churn, in terms of businesses leaving, wasn't as big of a pain point. The bigger issue was the downsells, which was an invasive problem. We incentivized the team to attach more products, but didn't necessarily have a clawback mechanism. If you sold five modules to a customer and they downsold three of them several months later, the salesperson would still get paid. - Former Director of Strategy & Operations, Toast

The executives estimated ~70% of the reported churn was driven by customers downselling, not churning to competitors. This highlights a misalignment between sales incentives and customer activation. Sales reps leaned on "three months free" promotions to drive conversion, increase ARPU, but for products that the customer often didn’t require:

A customer who doesn't activate and adopt a product is five times more likely to downsell that product. The promotions that we used, although successful, encouraged this behavior. From an onboarding perspective, we wouldn't put as much effort into onboarding some products versus others.- Former Director of Strategy & Operations, Toast

Once the core POS was live, getting a busy restaurant operator back on the phone to set up payroll or online ordering is difficult. Online ordering, payroll, and gift cards were the modules most impacted because they all require separate onboarding sessions to train customers.

A Former Manager of Customer Success at Toast, who led a team of 8 CSMs managing ~$15M in SMB ARR across the West Coast, described how the CS team tried to catch it before it happened:

90% of our day was focusing on QBRs. We're looking at activation and adoption. Is the product on and functioning? Have they had X amount of transactions? If you're paying for something, even if it's in a bundle, and you're not using it, that runs the risk of being churned. - Former Director of Strategy & Operations, Toast

Her team tracked customer logo churn at ~2.2% and gross dollar churn at ~6.5%, for her region on the West Coast. The East Coast was worse — ~4% customer churn, ~10% product churn. Seasonality drives churn differences across regions.

What's notable is how Toast tried to solve the problem of customers churning off modules. The Strategy & Ops team implemented sales clawbacks, eliminated the default "three months free" offer, consolidated invoices so bundled products appeared as a single line item rather than individually removable charges, and kept salespeople involved through onboarding. A Former Chief of Staff and Sr. Director of Hardware Operations at Toast, who supported the 1,000+ person customer success organisation, described the shift:

The main approach was no more three months free. The customer has to be bought in with some value from the beginning. The main thing was stopping that sales approach, and then making sure that if customers had something on their contract, they got activated on it within a certain amount of time. There were a lot of metrics around activation; it wasn't just POS activation. Everything had to be activated within a certain amount of time. - Former Director of Strategy & Operations, Toast

Since the churn issues reported in 2023/24, Toast’s improvements led to 100-200bps of churn improvement in pilot markets. But also reduced upfront attach by ~10%:

The debate was kind of like, are we okay being a gym? Gyms are fine having a bunch of zombie members who don't show up but still pay. That was always the question for us. In which case, just attach as much as you can upfront and be okay knowing that you're going to get a good amount of churn. - Former Director of Strategy & Operations, Toast

Once a customer has been oversold, failed to activate, and churned off a module, the growth sales team found it nearly impossible to re-sell that same product later. This caps the long-term NRR opportunity in the installed SMB base. Competitive churn remains negligible (sub-2-4%), and the physical stickiness thesis holds. But questions remain over the amount of unactivated modules still in Toast’s system.

Related Content

© 2026 In Practise. All rights reserved. This material is for informational purposes only and should not be considered as investment advice.