Weekly Update: Markel Insurance, Lam Research, Adyen & Agentic Commerce

Published Last Week

Markel Insurance Reorganisation

We recently published three interviews, one with CEO Tom Gayner, as part of our exploration of Markel’s recent insurance reorganisation. Markel is particularly interesting to us given its durable business model.

Markel has three engines driving return: underwriting income, wholly-owned subsidiary cash flow, and investment income. Even at higher combined ratios, combining these businesses under one tax-efficient roof is an effective way to compound capital. It’s also highly scalable, as proven by Berkshire.

In our interview with Gayner, we explored why Markel recently sold its reinsurance book.

We tried but couldn't make it earn the returns that it needed to continue to remain part of the group. I think there are a variety of reasons for that. Reinsurance, by definition, is one degree of separation removed from making the decision at the primary line. Your ability to control your destiny is at least diminished in some degree by the fact that you are one step removed from the action. That is not a fatal flaw. There are a lot of people who have run good reinsurance businesses for a long period of time, but it takes a certain size and scale and skills to do that specifically. We tried and we continued for several years. Basically, we kept raising the price per unit of risk, which is the directionally correct thing to do. But the way the ball bounced, whether it is US court systems or social inflation or loss cost trends, the risk kept getting more expensive through the last four or five years in such a way that we were never able to catch up and get to the point where we were charging enough per unit of risk. - Tom Gayner, Markel Group CEO

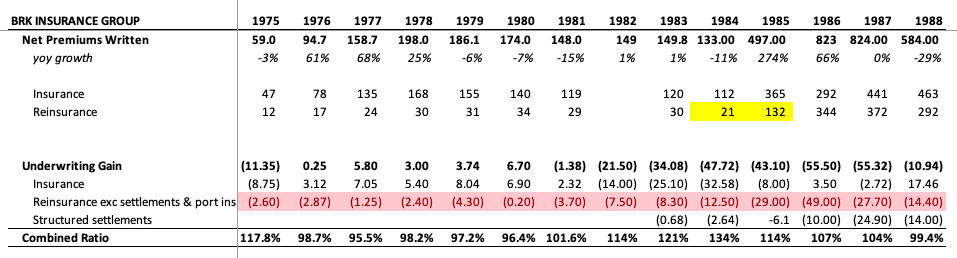

Markel’s reinsurance struggles led us to explore how Berkshire scaled its reinsurance business in the early days. Berkshire lost a ton of money writing reinsurance through the 70s and 80s.

However, what's missing above is that rates were 10-15% during this period. Insurers were writing at 105%+ combined ratio to invest in 15% government bonds. The low-rate environment today is much less forgiving.

Another unique characteristic of Berkshire is its overcapitalisation. Even since the 80s, Berkshire’s gross written premium to equity surplus is comfortably below 20%. For every $1 of premium written, there is $5 of surplus. Typical insurers run at ~80%. The difference is partly due to Buffett shifting from an investment manager within an operating company to an insurer. Berkshire’s overcapitalisation allows it to invest more of its float into higher-yielding assets and take greater and more unique reinsurance risk.

One interesting case study that brings this to life is the Fireman’s fund reinsurance deal Berkshire signed in 1985 (see the jump in reinsurance premium in yellow highlighted cells above; which also coincides with an investment in GEICO). In September 1985, Berkshire entered a 7% quota-share reinsurance treaty with Fireman’s Fund. For every $1 of P&C insurance Fireman’s Fund sold, BRK received 7c of premium in return for wearing 7c of all future claims. This was a deal between Buffett and Jack Byrne, who previously saved GEICO from bankruptcy. Berkshire backstopping 7% of Fireman’s Fund business helped its IPO as it was spun out of American Express that year. Not many other insurers could step in to provide such coverage at scale.

This deal gave Berkshire what it needed: float at scale. The Fireman’s Fund deal multiplied its insurance business overnight without requiring any insurance sales agents. A portion of this float was invested in Capital Cities / ABC and the rest is history.

While Markel has exited reinsurance, and many doubt its US insurance underwriting capabilities, its long-term underwriting track record is consistently profitable. Arguably Markel can afford a higher CR given its other two engines drive higher earning power than the typical specialty insurer:

If you look at the history of Markel from the IPO until last year, the average combined ratio over those 39 years is approximately 95. We have been able to compound the capital of the Markel Group for 39 years in the mid-teens rate with an average combined ratio of 95. - Tom Gayner, Markel Group CEO

One criticism of Markel Insurance in the US is its lack of brand or differentiation; some perceive Markel to mainly be a provider of excess capacity:

For Markel, it would be interesting to poll users to understand their perception of the value proposition. I would suggest that Markel primarily provides excess capacity, which is fungible. If I'm writing a 10X of 50 layer on a big commercial umbrella policy, next year someone else could easily replace me. There's no unique value proposition; I'm just offering capacity. As an excess player, I'm not relied upon to draft or manuscript coverage. My products are generally excess, so there's nothing proprietary about them. My product differentiation and capacity are commoditized. - Former Senior Executive at Markel Insurance

Markel is also perceived as more of a sales-focused insurer rather than a rigorous underwriter:

wholesale brokers enjoy spending time with Markel people, and they make the most of it…if you're taking these guys to the football game, can you get a couple of points on the next deal or something like that? They're polite and not the best negotiators per se, but they're fun people to party with. I think that's another thing because it's easier for a broker. A broker is pretty good at getting the deal done, right? They might say, "Hey, thanks a lot for taking us to dinner the other night. I've got a submission for you." It might be a poor submission, but the underwriter feels good because the broker likes them after going out to dinner. It's a human nature thing, and it's still a people business. If you ask most brokers, they'll say, "Oh yeah, I like Markel. I like doing business with them. They're nice people and easy to get things done with." Whether that's a good thing or a bad thing, I don't know. - Former Senior Executive at Markel Insurance

Last year, Simon Wilson, Former Head of Markel International, was hired to run US insurance to drive more accountability through the business. He reorganised the business into smaller, more decentralised teams with P&L responsibility. Perspectives of Markel's insurance reorganisation can be read in the following:

This interview with a former SVP at Lam Research, who spent over a decade reporting to the CEO, believes we’re entering the second phase of the AI capex cycle which will drive significant incremental demand for NAND:

I think we're now entering a second phase of that era in terms of semiconductors, where it's going to start driving the NAND side as well. There are plans to couple what's called HBF, high bandwidth flash, with HBM and dramatically increase, by 10x, the amount of memory on a chip available for AI models. The cycle is still gaining momentum at this point; it's not leveling off. - Former SVP at Lam Research

Lam is a critical supplier in this value chain:

Lam is a very critical supplier in 3D NAND because they own three critical steps: putting the stack together, drilling the hole in it to connect all the stacks together, and then filling the hole. They have a commanding position in all three of those. The world is going to be very constrained by Lam if the NAND capacity takes off strongly and they are demanding more from Lam; Lam is going to be stretched trying to add significantly to their 2026 capacity plans. - Former SVP at Lam Research

This interview can be read alongside the following:

This interview with a Director of Growth Products & Partnerships at Visa, who previously worked at Adyen on strategic partnerships with Apple Pay and Google Pay, provides a perspective on the risks and opportunities in the checkout process as agents potentially begin executing transactions.

One question is whether agentic payments can drive volume whilst maintaining the underlying payment infrastructure incumbents have built over years:

For me, agentic payments is exciting for the space, not necessarily because it disrupts how traditional rails work today, but more so because it turbocharges it and reduces the friction that we see today in payments. The bet that a lot of people are placing in the industry is that more consumers at the top of the funnel, the discovery phase of the shopping experience, will find that whole process becomes much easier. We'll see increased volume of payment transactions as a result of agentic. But once the agentic transaction executes, everything that flows behind the scenes should still work in the way that we're used to today in terms of fraud checks, authorization checks, and so forth. — Director, Growth Products & Partnerships, Visa

Today’s solution seems to run on top of standard rails:

"A lot of what is being built now for agentic commerce is taken from the standard rails. You can generate a token for your AI agent. That token can be identified -- this was Claudio's token, it is related to this card, and this is the context you can use it. You can set spending limits and even categories. MasterCard, for example, allows you to set, 'Use it for shopping for clothes, but don't use it for high-value items like jewelry.' Agents can hallucinate and do a lot of weird things, so being able to constrain that is quite helpful." - Former Engineering Director at Adyen

This view from a customer provides an alternative perspective on the current state of agentic commerce:

"I would take what has been going on with a big portion of salt, not just a grain. Everyone is trying to be first and be known. Stripe launched with OpenAI on Etsy. Adyen partnered with Gemini. The funniest thing is that the whole buzz is around the merchants and providers, but the end user still needs to be educated and gain trust... I was at an event and we saw a presentation where they asked ChatGPT to buy a pack of white socks. It took 15 minutes and it was crashing.

This can be read alongside the following interviews:

Related Content

© 2026 In Practise. All rights reserved. This material is for informational purposes only and should not be considered as investment advice.