AWS vs OpenAI, CoStar, & Constellation’s AI Risk

Given the growth in interviews we’re publishing and to save this email becoming one long list list, we’re only listing a selection of 25 interviews per week. If you wish us to publish all interviews, please reach out and we will revert back to the old format.

Published Last Week

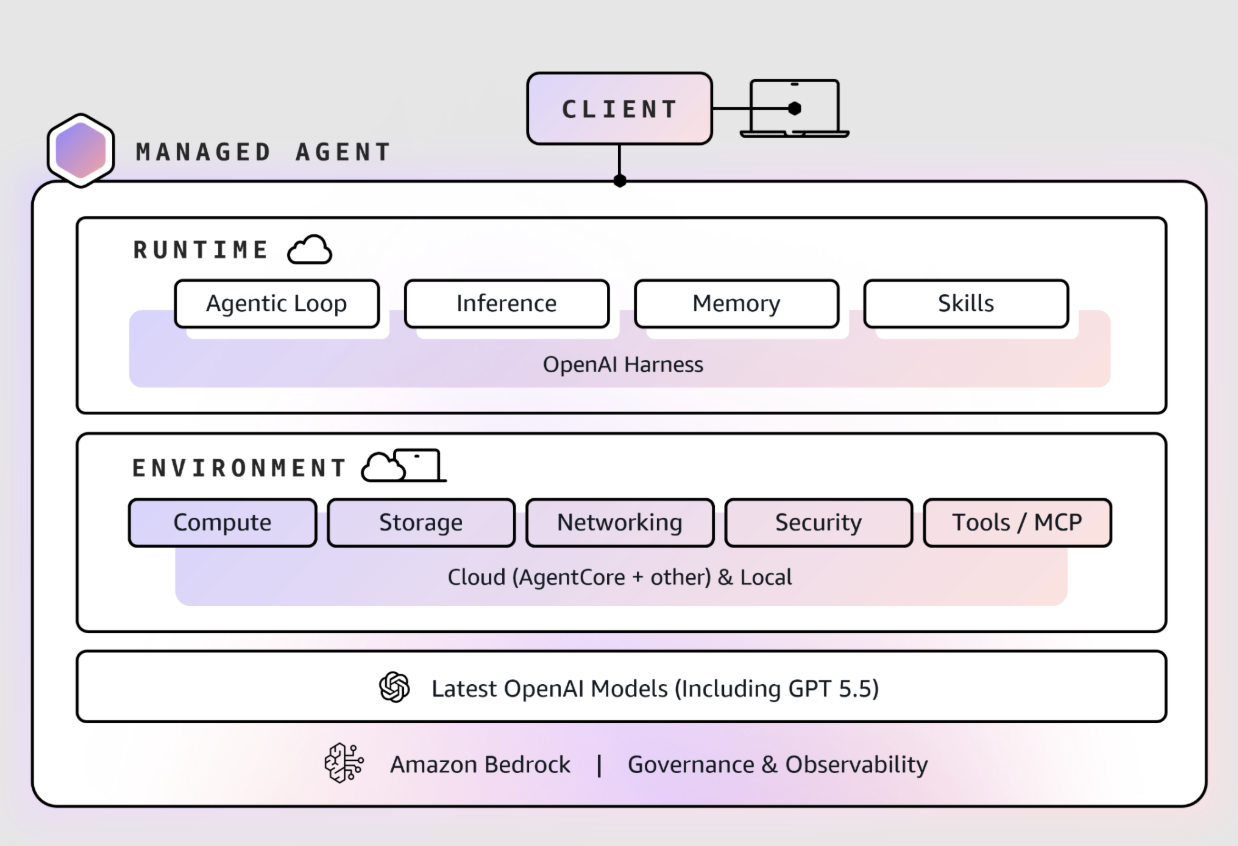

AWS and Bedrock Managed Agents

AWS recently extended its partnership with OpenAI to exclusively offer “Managed Agents on Bedrock”. AWS provides the permissioning, governance, security, and underlying compute and storage infrastructure; OAI provides more of the harness and intelligence.

This new Bedrock service builds upon AWS’ deal with Anthropic to distribute Claude API to AWS customers. In Q1 26, AI hit 10% of total AWS revenue, of which nearly 40% is from Bedrock. Anthropic is potentially driving an estimated ~80% of Bedrock revenue:

We have observed, out of, say, a billion-dollar revenue of Bedrock, I would estimate 80% could be attributed to Anthropic. The remaining 20% is split between other providers like DeepSeek, Llama, and Cohere, even AI21 - Former Generative AI Director at Amazon Web Services

In a recent interview, Altman made an interesting comment:

"Hard to overstate how critical it is. I no longer think of the harness and the model as these entirely separable things. I would also suspect that model and harness come together more over time and I would expect that pre-training and post-training eventually come together more over time as well. - Sam Altman, Stratechery, Apr 28 2026

Agent runtime, tools, memory, and model are collapsing into one product. Bedrock Managed Agents is OpenAI and AWS co-building this product. This is different to AWS’ Anthropic deal which resells Claude via Bedrock API to enterprise developers building custom apps. Both deals also have different usage of Trainium; over 50% of Anthropic’s Bedrock inference is on Trainium and OpenAI has 2 GW for its new Frontier enterprise platform on Bedrock.

While AWS will earn margin at the silicon layer in both deals, how the value and profit pool is carved up between the labs and AWS is a long-term question we’re exploring. As compute supply normalises and agentic adoption grows, a risk to AWS is that the model, harness, and RL feedback loop owned by the labs capture the majority of the incremental profit pool. Although there will likely be an explosion in compute demand, the risk is that the customer relationship and pricing power moves towards OAI and Anthropic.

Two simple questions come to mind:

- How much of an enterprise's agentic workflows will be run on EC2 and S3?

- And separately, how much of the volume and profit pool can Bedrock capture as compute supply normalises?

For example, can enterprises reduce AWS data gravity by moving or leveraging data outside of AWS for specific agentic workflows.

I'm even seeing this with some of the agentic stuff that we are building, where could it be the case that agents operate on a thinner or more limited set of data? If you're needing to hit up your operational or analytical database to get all the things from however many years ago, that's where data gravity is powerful. We're working on a use case where an agent has to look at the last two weeks of patient data. It made me think about that. We're doing real-time alerts, like, this happened, so you have to do this, or it will drive a workflow. But if it's based on recent data, could that change things over time? - Former Product Lead, AI at AWS

While training workloads have been diversifying towards Neoclouds, inferencing seems more difficult to move:

we're already seeing OpenAI diversifying the infrastructure they're using. Starting first with training, they're well down their path of diversifying where they're doing training. I would expect most of the training they're doing on someone like CoreWeave or other Neo Clouds is almost by and large training, because there are a lot of complexities in saying that's where inferencing will go. Where's the rest of the app? If they don't have all of the services for the rest of the app to run, then you're going cross-cloud, which introduces a bunch of complexities around latency, throughput, contractual commitments, support—everything gets a lot more complicated when the app is running cross-cloud. - Former VP, Azure AI Infrastructure, Optimized Workloads and Storage at Microsoft

This quote highlights AWS’ positioning as the 'durable middle':

On one end, you have the AI labs who are spending gobs and gobs of compute right now, along with what I would consider a couple runaway applications. And then at the other side of the barbell, you've got a lot of enterprises…And then in that middle of the barbell are all the enterprise production workloads…I think that middle part of the barbell very well may end up being the largest and the most durable. - Andy Jassy, Q4 25 earnings

This is different to both Microsoft and Google:

our core goal is to decouple the harness from the models and then have the context richness show through because customers are going to use multiple models. - Satya Nadella, Q3 26 earnings call

One of the things people don’t realize is we monetize many different parts of the stack in different ways. Like Anthropic, there’s a lot of labs that use our stack — in fact, most of the large AI labs use our stack. So if somebody uses TPUs to either to train their model or to use it for inference, we’re monetizing that part of the stack, that gives us resources to then fund our R&D and other investments. Some of the labs use our TPU and our Gemini model, others may use our TPU and then buy our cybersecurity protection for their models. So as a platform player, we have to allow our technology to be monetized in as many ways as possible and we don’t see it as a zero sum. - Thomas Kurian, Stratechery interview, April 2026

We explore this topic in various interviews including:

- AWS: Unit Economics, Infrastructure Scaling, and the AI Transition — May 2026, Former Finance Manager at AWS

- Microsoft Azure: AI CapEx Strategy, GPU Economics & OpenAI Contract Structure — Apr 2026, Former VP Azure AI Infrastructure at Microsoft

- Microsoft AI: Enterprise Sales, Copilot Adoption & Distribution Moat — May 2026, Former Senior Director AI at Microsoft

- Microsoft Dynamics 365: Winning Back Salesforce Customers with Copilot & ROI — May 2026, Former Senior Director AI at Microsoft

- AWS Bedrock vs Microsoft Copilot: Enterprise AI Integration & Competitive Positioning — Apr 2026, Former Product/Strategy Lead, AWS Agentic AI

To better understand Constellation’s portfolio, we analysed and tagged nearly 1,000 subsidiaries based on the following characteristics and product attributes:

- Regulatory end market: sells software to customers within a regulated end market (banking, insurance, healthcare, government, social housing, utilities)

- Payments: facilitates transactions to the vendors' customer

- Financials: has a core financials module; chart of accounts, accounting, etc

- HR / Payroll: runs payroll for customers

Proprietary data is another potential customer lock-in but we excluded this as it’s more nuanced to analyze from the outside. We believe software systems of record with the attributes above are somewhat more protected in customers switching than those without. Our research suggests the following:

- ~69% of companies are serving regulated markets. By revenue, this is closer to ~85% given large businesses like Altera and Trapeze are not revenue-weighted.

- ~45% of the businesses have at least one payment, financial, or payroll module

Our research goes on to share the breakdown of regulated markets, operating group split, and AI risks. This can be read alongside the following interviews:

We also published two CEO reference checks as part of our new add-on subscription service studying the character and culture of leaders of companies we're following.

In 1986, Andy Florance founded CoStar Group in his Princeton dorm room and continues to lead the company today. His controversial leadership style and the culture at CoStar have been reported for a number of years. The company has been a target for activist investors who think the Homes.com investment is value destructive.

We have interviewed executives that have reported directly to Andy Florance over the past 15 years to get a better understanding of how his leadership style affects how the business operates.

- Former Senior Executive at Homes.com: Spent over a decade working at the company.

- Former Senior Executive at LoopNet: Spent a decade at LoopNet and built out the go-to-market strategy.

- Former Executive at CoStar Group: Worked on multiple acquisition processes with Florance over half a decade.

- Former Senior Executive at Apartments.com: Spent a decade at Apartments.com and was involved in selling the business to CoStar.

This can be read alongside the following:

In Q1 26, Amazon’s perishable item sales grew 40x YoY. Perishable items also made up nine of the top 10 items ordered for same-day delivery. Grocery has long been a category Amazon has tried to crack, and Doug Herrington, CEO of Worldwide Stores, has been at the forefront of the company’s consumables and grocery strategy for over a decade.

This IP management check aims to provide a glimpse into Doug’s leadership style, characteristics, grocyer, and Amazon’s culture. Our work is curated from interviews with multiple former colleagues of Doug’s including:

- Former President at Amazon: spent ~10 years at Amazon, ran a $20bn P&L inside retail, and reported to and worked alongside Doug.

- Former VP at Amazon: spent over a decade at Amazon in consumables before being promoted to work on Special Projects with the S-Team.

- Former VP at Amazon: the executive spent nearly 8 years at Amazon launching and running its B2B business.

- Former General Manager at Amazon Grocery; spent a decade at Amazon and reported to Doug.

- Former VP of Amazon, Finance: worked with Doug on reporting and OP1 and OP2 budgeting processes.

Former Technical Advisor at Amazon : executive was a technical adviser to senior management at Amazon and was involved closely on how Doug and senior management train new leaders.

This can be read alongside:

- Amazon Fresh, Whole Foods, & US Online Grocery — Former Head of Launch Management at Amazon Fresh

- Amazon: Deconstructing the Retail P&L — Former Finance Manager at Amazon

- Amazon Retail: 1P vs 3P Economics — Former General Manager at Amazon

- Amazon vs Temu: Business Model & Logistics — Former Senior Manager at Amazon Logistics

- Amazon Robotics: Sparrow & Warehouse Cost Efficiencies — Former Head of Systems and Products at Amazon Robotics

- Amazon FBA & 3P Sales: A Seller's Perspective — Amazon Third-Party Seller for 16 years

We now have the following reference checks completed that are available standalone or as a bundle:

Related Content

© 2026 In Practise. All rights reserved. This material is for informational purposes only and should not be considered as investment advice.