Google Gemini, Azure GPU Planning, Toast, CCC's AI Risk

Here is a selection of interviews published last week. Visit our platform for all research published.

Published Last Week

Microsoft GPU Planning: Amy’s got the power

As part of our research on hyperscaler positioning in the AI stack, we interviewed a former leader of Azure AI Engineering at Microsoft. Before exploring the risk to hyperscalers like AWS and Microsoft, one interesting takeaway on GPU capacity planning is not only how Microsoft prioritises capacity between OpenAI, Copilot, and Foundry, but just how much power Amy Hood has internally. Amy is the GPU boss:

Amy Hood was the GPU czar so she approved every single GPU…It is a simple "show me the money"—here are the GPUs you need, how much revenue are you going to produce, what is the gross margin of the service, what is the EBIT margin, what is the average dollar per GPU? That is the bottom line. - Former General Manager, Azure AI Engineering at Microsoft

You could not have GPUs running idle. We were constantly getting hammered on GPU utilization. When utilization went down to below 60% on a cluster, those GPUs would be reallocated to different teams because everyone was always screaming for capacity. The only way you can make money on this business is to get fleet utilization above 60%. That is the break-even point. - Former General Manager, Azure AI Engineering at Microsoft

The majority of the interview explores the risk of Azure and AWS becoming bare metal providers to labs:

The only way that OpenAI and Anthropic can push past IPO is to abstract all the platforms down to bare metal. As OpenAI has done with Oracle and Stargate, they are using them as a bare metal GPU-as-a-service provider. That is exactly what Microsoft is doing with neoclouds. What Amazon and Microsoft become to OpenAI and Anthropic are GPU-as-a-service providers, straight capacity. Anthropic deals where you provide me capacity, I pay you per hour, and I license the models back to you. With OpenAI and Microsoft, there are the complexities of unwinding the deal that they have had. That is what it is coming down to - winding down the IP access, then becoming straight licensing. - Former General Manager, Azure AI Engineering at Microsoft

This perspective on open-source is also interesting. At the workflow level, open-source models may win the simple, routine tasks. But these have arguably always been commoditised and the profit pool is unclear. More complex, value-added workflows may remain a 3-player frontier model game where the majority of returns on capital flow:

When you are an enterprise customer, it is less expensive to use the Foundry, Bedrock, or Gemini agentic platform to build an application using an open source model. You can get any open weight model from Foundry because everything is there. As a commercial customer, it makes perfect sense to use mixture of experts and open weight models for routine tasks like summarization or a very constrained RAG-based chatbot. But for any kind of fraud detection or detailed report writing and analysis - any high-value work that is going to impact cost or generate revenue is going to be done on frontier models. The bottom line is if there was money to be made in open weight models, OpenAI and Anthropic would have released one. The same goes for mixture of experts models. There is simply no money to be made on it. - Former General Manager, Azure AI Engineering at Microsoft

The interview goes on to explore the biggest mistake Satya has made, his relationship with Altman, and how Azure is positioned vs OpenAI and Anthropic. It can be read alongside:

- Microsoft Azure AI: Capacity Planning, GPU Allocation & Internal Prioritization — Former General Manager, Azure AI Engineering at Microsoft

- Microsoft Dynamics 365: Winning Back Salesforce Customers with Copilot & ROI — Former Senior Director, AI at Microsoft

- Microsoft AI: Enterprise Sales, Copilot Adoption & Distribution Moat — Former Senior Director, AI at Microsoft

- AWS Bedrock vs Microsoft Copilot: Enterprise AI Integration & Competitive Positioning — Former Product and Strategy Lead, AWS Agentic AI at Amazon

- Microsoft Azure: AI CapEx Strategy, GPU Economics & OpenAI Contract Structure — Former VP, Azure AI Infrastructure, Optimized Workloads and Storage at Microsoft

Google Culture, Gemini, & the AI Harness Layer

This interview with a Former PM at Gemini, with nearly a decade building AI products at Google, explores how the AI harness layer is evolving.

The majority of the effort today is moving away from model to harness and infrastructure. Everybody is short on chips. The way you can own the end-to-end manufacturing, the optimization of using these accelerators, and building the middleware to run these models with optimizations has a lot of value. When we did Gemini, just getting the model speed up by 10% was huge, considering the entire global fleet… Anthropic is leading with their managed agent offering, and Google is doing Antigravity harness. These are the places where you have to co-develop with the model and make things extremely good. That's what the end user is going to feel and they're willing to pay for it. - Former Group Product Manager, Gemini at Google Cloud

And how the harness layer may get thinner over time as models improve. As the harness thins, does the model layer capture more of the value? And where does it leave those without leading models?

These things are getting thinner as the model gets better. Today, people have to put in a lot of work into harness because the model isn't there yet. We know models hallucinate. The model is subject to noise a lot. If you have irrelevant information or conflicting information, unlike a human, the model gets confused. But this is getting better over time. I would predict the harness layer is going to get thinner over time. The overall prediction is that it becomes like a utility - Former Group Product Manager, Gemini at Google Cloud

We also published an interview with a Former Google Product Manager, with over 13 years experience at the company, on the culture across different Google organisations and how it has changed over the years:

if you looked at Google Cloud versus Google Core and Search, I remember at one point somebody on one of my peers' teams was having performance challenges. I spoke to my VP and my VP said, "He's not going to cut it here in Search. Maybe he could go work for Cloud." There was this perception that Google Search is hiring top-tier people. Actually, we didn't care if they knew Search or anything specific to Google. We cared if they were smart and able to be good. Whereas Cloud was hiring people with Kubernetes experience, and as a result, the bar in caliber was considered lower. - Former Group Product Manager, Google Search at Alphabet

These interviews can be read alongside the following recent GOOG interviews:

- Google Gemini, Anthropic & the AI Harness Layer — Former Group Product Manager, Gemini API at Google Cloud

- Google Search: Culture, ChatGPT Panic & AI Overrotation — Former Group Product Manager, Google Search at Alphabet

- Broadcom & Google TPU: SerDes IP, Power Efficiency & Vertical Integration Strategy — Semiconductor / SerDes IP expert

Toast vs Square (and DoorDash)

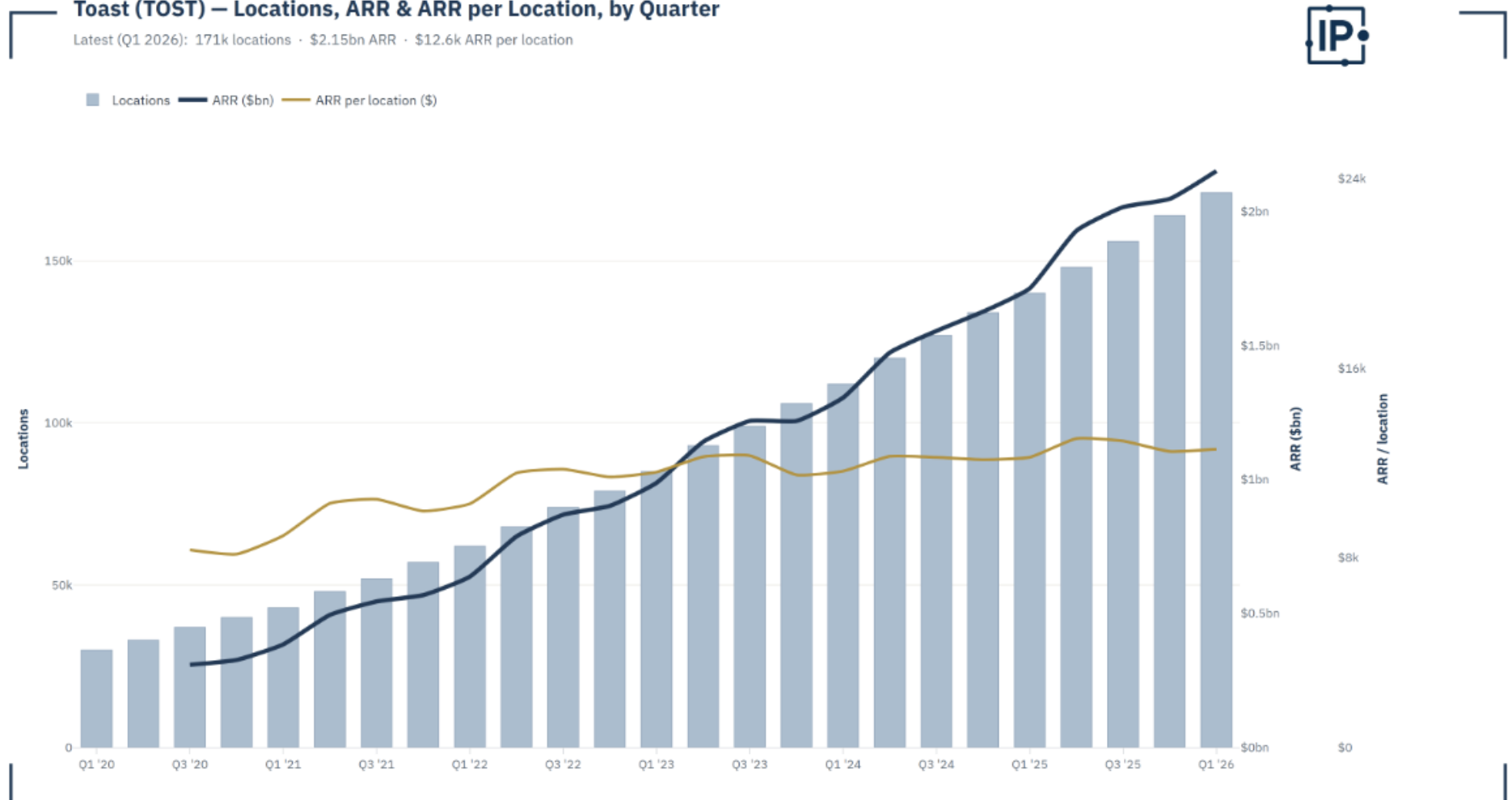

Over the last 14 years, Toast, the restaurant POS software provider, has grown to 20% market share of US SMB Restaurants.

Toast has gained market share by replacing legacy systems and competing against payment-centric companies whose software and hardware products were inferior to Toast, especially in full-service restaurants.

Toast started with higher complexity restaurants, full-service ones where you need to manage tables, reservations, waitlists, and have coursing in the back of the house. There's a lot of front-of-house and back-of-house technology in a full-service restaurant. This allowed them to deeply understand one segment and succeed before moving on to others. — Former VP of Product at Toast

Toast's products' quality is definitely superior... The integrations, the partnerships and capabilities they have. That would be number one, and I think every company is building AI into their technology, but Toast was building it into the platform a lot sooner. — Sales Executive at SpotOn

The legacy systems, Micros and Aloha, are old and terrible. If you owned a restaurant, you were stuck in your office at least 12 hours a day because the system was on-site. They came in with a cloud approach, which means business owners are not stuck in one location and can do software updates and manage things remotely. They are MIT engineers so they are smart people. - Sales Director at SpotOn

Interestingly, Toast has won 20% market share whilst also charging ~25% higher TCO for a typical SMB restaurant:

I would say Toast, total cost of ownership, in the long run, like a two-year contract with Toast, is probably 25% higher. - Former Enterprise Account Executive at Square

However, our conversations suggest competitive intensity is rising. Competitors like Square, SpotOn and Clover are significantly cheaper than Toast on both payment and SaaS fees, while Toast aggressively discounts hardware.

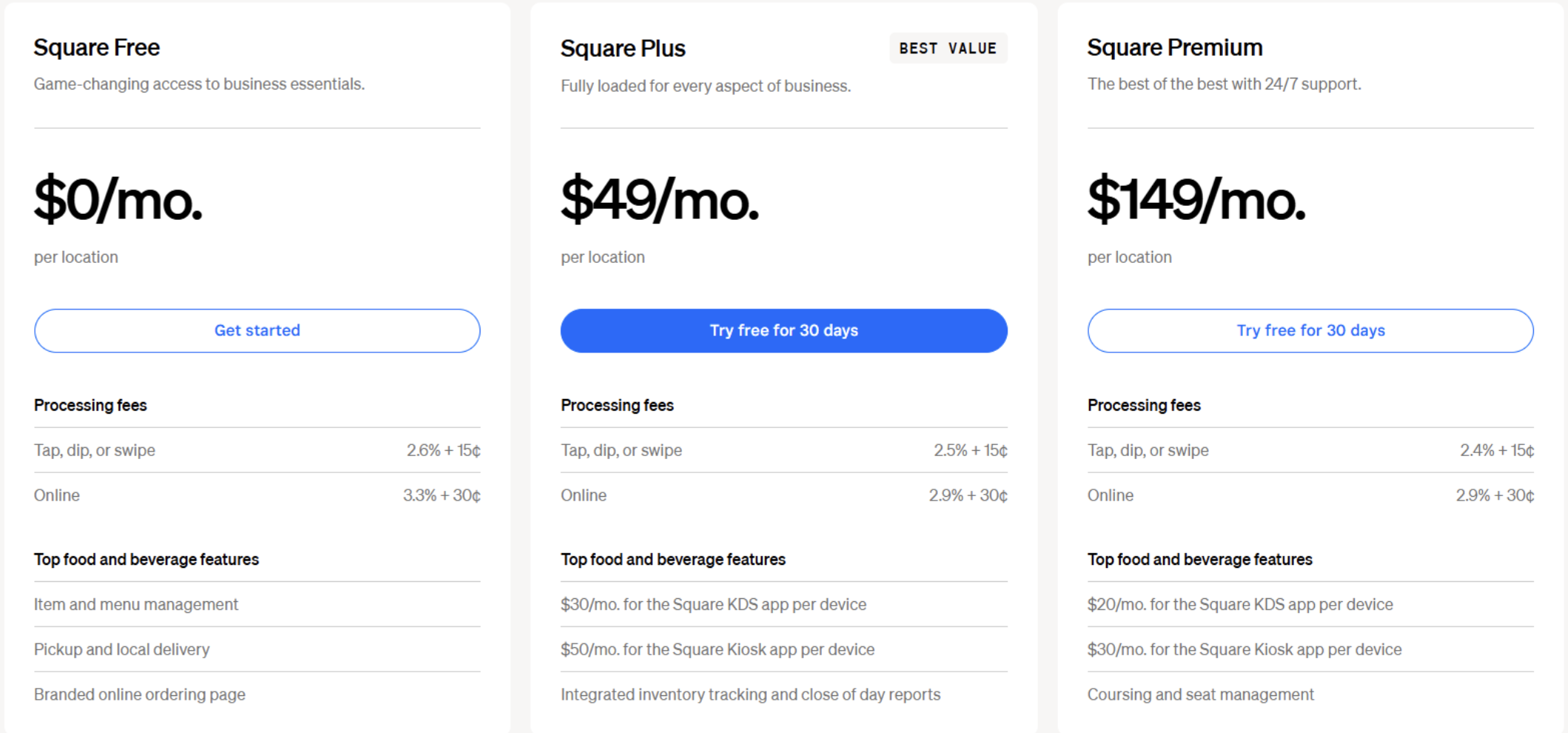

Square for Restaurants pricing page:

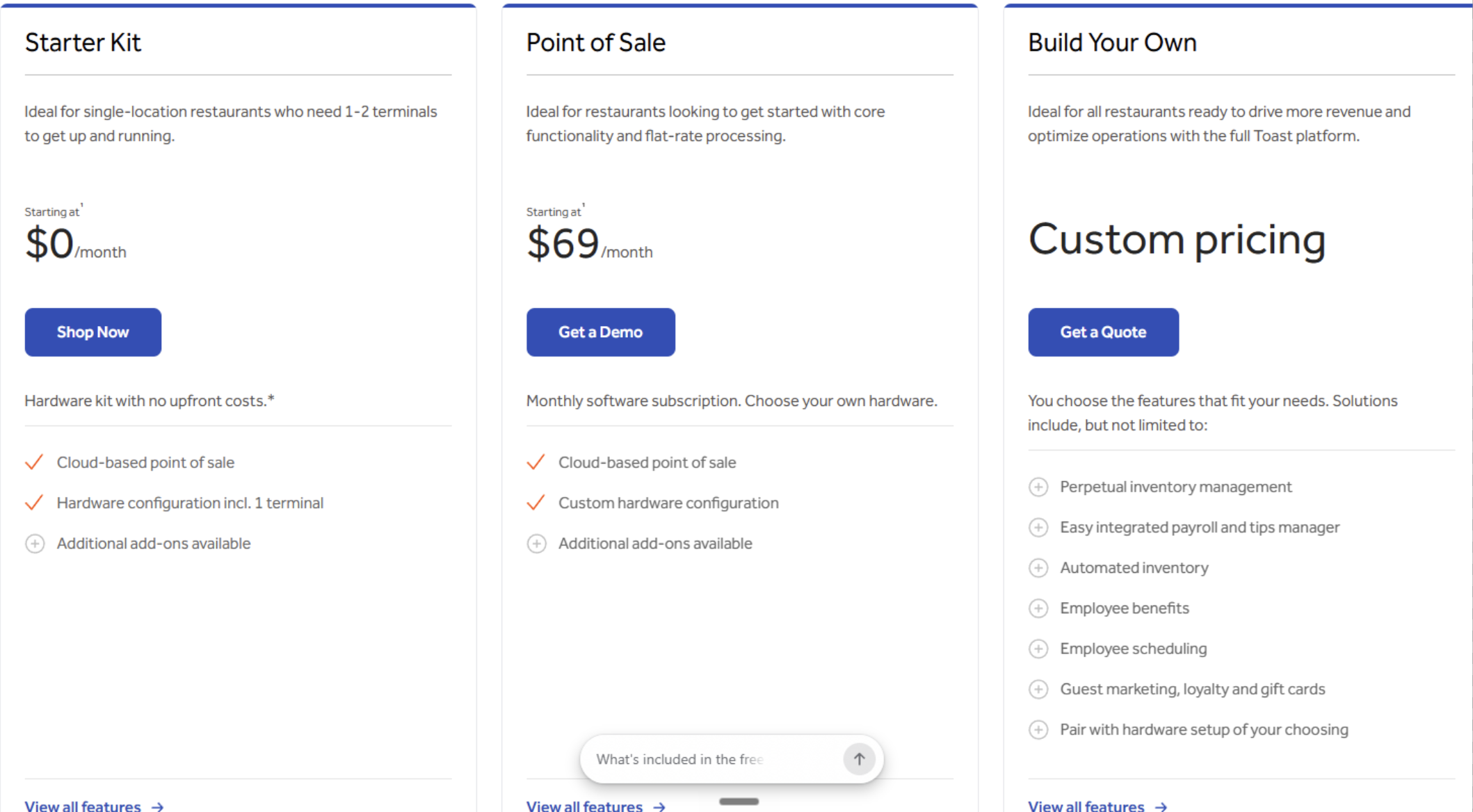

Toast pricing:

Toast makes roughly $500-$600 per month in subscription revenue per average location. Square is charging 4-5x less with loyalty/marketing, staff management, online ordering included:

Square's strategy is to make money on the payment processing and offer everything else at as close to cost as possible... Around Q2 of last year, Square did a repricing strategy to dramatically lower its SaaS. The objective was to undercut everyone on SaaS... Square predominantly makes its margin... given that it is the bank and is not sacrificing points of margin on processing to external acquirers. — Partner Manager at Restaurant365

We have such great margin on our processing that we could really still come in under Toast but make profit. — Former Sales Executive at Square

Square has also moved from an inside sales motion to a field sales motion to replicate Toast. The company supplements field sales with ISO / VAR relationships to add more boots on the ground. The company is seeing product improvements after hiring a former Product Management VP from Toast in 2023.

It was only around three years ago, when Ming-Tai Huh—formerly a product director at Toast—was recruited by Square to lead its food and beverage product division, that Square began to significantly accelerate its investment in best-in-class restaurant software.— Partner Manager at Restaurant365

Mid-2024 is when things started to get moving. Beginning of 2025 is when they started to expand the field sales efforts much more. - Former Enterprise Account Executive at Square

Square's strategy seems to have paid off so far.

GPV from food and beverage sellers was up 21% year over year, our strongest growth rate since the first quarter of 2023, while GPV from retail sellers and services sellers grew 11% and 7% year over year, respectively. We saw a more pronounced acceleration in year-over-year growth for our mid-market seller segment (>$500K in annualized GPV) compared to our other seller segments during the first quarter. - Block Q1 2026 Shareholder Letter

While Toast is expanding upmarket, horizontally (retail, hospitality) and internationally simultaneously, Square is attacking them in their core market. This doesn't even count DoorDash, which has proven itself strong at product & execution and has a lever to pull with commission rates and its existing distribution...

This work can be read alongside other recent Toast interviews:

- Toast: Marketplace Partnerships, DoorDash Competition & Revenue Share Economics — Former Partnerships Executive, Toast

- Toast: Territory Sales Structure, Compensation & Product Bundling Strategy — Former Territory Sales Rep, Toast

- Square vs Toast: Payment Margins, Software Pricing & Total Cost of Ownership — Former Enterprise Account Executive at Square

CCC's AI Risk

CCC is an interesting example of the potential risk of AI. CCC aims to combine proprietary data with software switching costs. The company offers a software platform for P&C insurers to process auto claims efficiently.

In 1980, CCC started by collecting used and new vehicle pricing from dealers to help insurers price the residual value of the claimant's vehicle. The residual value is critical for the insurer to determine which vehicles are a total loss vs repairable. This is from the 1980 filing:

Dealers would ‘contribute’ pricing data in return for having the opportunity to sell to or buy cars from the claimant. CCC still has a robust total loss valuation product and has also moved into estimating repairable vehicles. This is where AI comes in.

When a claimant crashes, they send a photo to their insurer who uses CCC to determine an estimate of the damage. CCC's software covers every step of the claims process: CCC Workflow, an insurer claims processing software platform, and CCC One, an ERP for repair shops, are critical tools for the end-to-end claims process. Each claim can have ~100 touch points between the insurer, repair shop, OEM, tow and salvage providers. CCC is at the centre of it all.

CCC has ~85% of the estimates market; it reports it has over 1bn photos covering $2trn of repairs. In the claim estimation process, the proprietary data is arguably both the closed loop of repair estimates, the repair process, and the actual repair values.

But an interesting part of the proprietary data is the photo of the crashed vehicle. And CCC doesn’t strictly own the photos:

Repair facilities and the insurance carriers own the photos. They give CCC the rights to use them, but not every carrier does. - Former Senior Leader at CCC Intelligent Solutions

And now AI can produce estimates that are ~5% from CCC estimates:

CCC built models, and everybody's assumption is that they are so proprietary that public models cannot possibly be good enough to use. In fact, in July of 2025, we did a test against OpenAI, and it was within 5% accuracy of our own models. - Former Senior Leader at CCC Intelligent Solutions

This opens up all kinds of questions around switching costs, pricing power, insurers building in-house, etc. We walk through all these risks in the interview with a former senior leader at CCC and also explore why the company has struggled to see material AI revenue growth even though it claims to have been working on AI for a decade.

This interview can be read alongside our work on CCC:

- CCC Intelligent Solutions: Proprietary Data Moat & AI Risk — Former Chief Technology Officer at CCC Intelligent Solutions

- CCC vs Mitchell: Casualty vs Auto Physical Claims Process and Costs — Former Senior Vice President at GEICO

- CCC vs Mitchell: Collision Repair Estimation Software - Former General Manager at Service King Collision

- CCC Intelligent Solutions Moat & Competitive Threat — Former Product Leader at CCC Intelligent Solutions

- CCC Intelligent Solutions vs Mitchell: Estimate Data Quality — Former Senior Director at CCC Intelligent Solutions

Related Content

© 2026 In Practise. All rights reserved. This material is for informational purposes only and should not be considered as investment advice.