Bruker: Inventory write-downs classified as restructuring charges

An inventory writedown is supposed to do one thing: drag your gross margin down. You bought stuff to sell, you couldn't sell it, the cost lands in cost of revenue, your margin suffers.

But GAAP gives the issuer a choice about where to land the charge.

- Land it in cost of revenue. GAAP gross margin drops, and non-GAAP margin drops with it.

- Land it in restructuring. Gross margin is unchanged. Non-GAAP margin — the one investors track for the underlying trajectory — actually goes up, because non-GAAP excludes restructuring. The charge is recorded, but in a part of the P&L most investors skip.

Which classification is appropriate is a judgment call. Inventory that won't sell looks like a cost of selling things, while restructuring is the line for structural events like factory closures or segment divestitures.

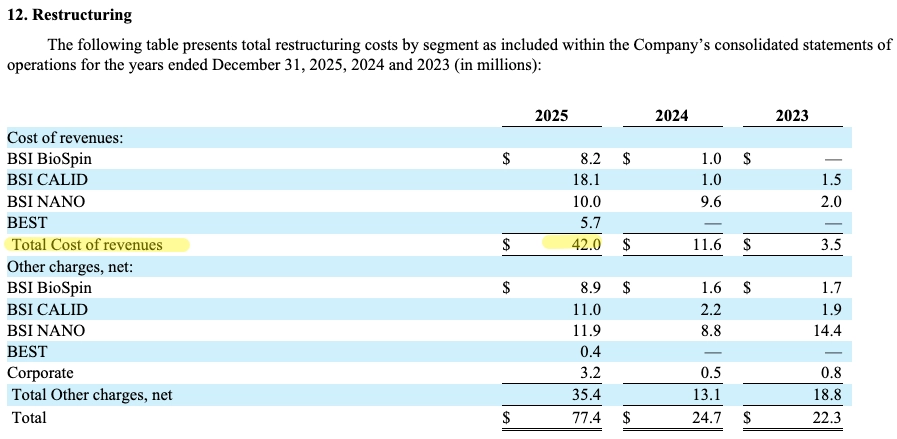

In its FY 2025 10-K footnotes, Bruker records $25.8 million of inventory under the heading "scrapping, expired, or expiring inventory" — 5x the $5.5 million in FY2024 — within restructuring. Total restructuring charges booked inside cost of revenues moved from $3.5M in 2023 to $11.6M in 2024 to $42.0M in 2025.

Three details from the Restructuring footnote are worth investors’ attention.

Free Sample of 50+ Interviews

Sign up to test our content quality with a free sample of 50+ interviews.

Related Content

© 2026 In Practise. All rights reserved. This material is for informational purposes only and should not be considered as investment advice.